Peloton: Remote Leverage

In previous posts we have talked at length about the importance of leverage in business and business quality.

In fact, in the last post we talked about the implicit leverage provided by stock based compensation. I argued in that post that stock based compensation was actually good for companies because it is non-recourse, has the added benefit of aligning incentives of investors and employees within a company and can be viewed as a competitive advantage.

Whenever I look at a company, my first question is almost always, “Where is the leverage?” I contend that behind every good business there is a good leverage scheme. Conversely, behind every bad business is a bad or deteriorating leverage scheme.

Sometimes the leverage is easy to find as the company has a ton of recourse debt sitting right on the balance sheet like we saw with Carnival.

Other times it is sneakier. For instance, Medifast convinces its downline clients to extend it de facto bankruptcy-remote (remote to Medifast) credit. (My opinion, of course)

Today’s company is a curious case study in remote leverage. I’ll start by saying that I completely missed this one. A huge miss in retrospect.

Peloton Interactive

One of this year’s hottest stocks is undoubtedly Peloton Interactive. Just look at the chart. It is beautiful.

Coming into 2020 Peloton was viewed as a reasonably successful consumer product IPO with a niche luxury product. Many takes were made, but the most common was:

“Who has $2,500 for a stationary bike?”

I don’t like to admit being wrong, but I definitely said that exact sentence. And guess what? I spent $2,500 on a stationary bike!

Dubra in January 2020: “Who has $2,500 for a stationary bike?”

Dubra in March 2020: “Hi Peloton, yes I’d like the Bike Essentials package. Thank you.”

Great Success

Jokes aside, affordability was a legitimate question with Peloton. The argument was: There aren’t a lot of people who can or are willing to drop $2,500 on a stationary bike. As a result, the addressable market is capped and growth should begin to slow materially.

In January 2020, a lot of Wall Street was thinking that way, myself included. Peloton then went ahead and proved all of us wrong. As can be seen by the graphs below, subscribers and revenue promptly re-accelerated massively.

Coming into the year Peloton was growing subscribers 100% YoY and managed to re-accelerate that growth to a blistering 140%.

Similarly, revenue line items are growing at eyepopping rates. Connected Fitness Products (the bikes and treadmills) have accelerated from 72% in Q4 2019 to 282% in Q3 2020. Subscription revenue (the recurring monthly fee) accelerated from 112% in Q4 2019 to 133% in Q3 2020.

These are just insane numbers. It is no wonder the stock is up 5x+ from the beginning of the year.

Many of you are probably thinking the following:

“C’mon Dubra, the growth happened during a pandemic. People were stuck inside and there was an at-home fitness movement concurrent with this explosive growth.”

I completely agree with that point, but push back with affordability yet again. Wouldn’t affordability be an even bigger hurdle in a pandemic?

Somehow Peloton was able to overcome a very difficult economic backdrop to sell a luxury product to hundreds of thousands of people. The way they did it is fascinating. Frankly, it is the key to the Peloton business model, which I missed when I was a hater in January.

Remote Leverage

Peloton was able to sell 1 million luxury bikes in a pandemic and period of massive economic uncertainty. They did it through remote leverage.

Here is what that looks like:

Peloton has partnered with Fintech startup Affirm to finance hardgood (bikes and treadmills) purchases. And the deal is pretty good. It’s a 0% APR installment loan to the consumer.

Affirm’s financing arrangement is a game changer for the affordability question. Suddenly it isn’t $2,500 out of pocket up front. It is $2,500 out of pocket over the course of up to 39 months… That’s a big difference in the United States of Consumerism!

The average consumer calls that free.

What a great deal for Peloton. They take on none of the consumer credit, no balance sheet risk and their addressable market multiplies. This is a top tier use of OPM (Other People’s Money). In this case, it is Affirm’s money and more appropriately Affirm’s lenders/investors’ money (Other People’s Money x2).

Note that should this financing arrangement materially change, it could have a drastic impact on Peloton’s ability to continue selling more hardgoods.

Affirm S-1 Filing

How do we know Affirm has been driving a lot of the growth at Peloton?

Well, we didn’t. In fact, there was no mention of Affirm in Peloton’s IPO filings or subsequent 10-K and 10-Q filings, which is odd given the importance of this partnership to Peloton’s business model.

It only became apparent how important Affirm is to Peloton when Affirm filed an S-1 with the intention to IPO in the coming weeks.

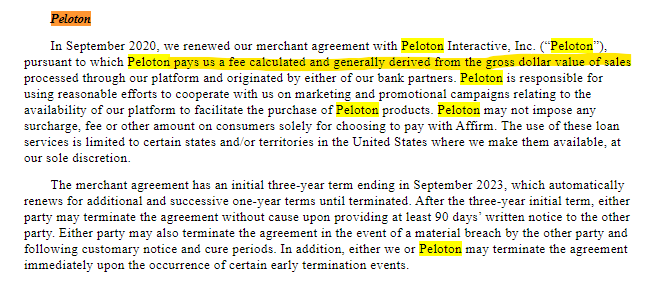

You can see from the Affirm S-1 that as of the September 2020 quarter, 30% of AFRM’s revenue is derived from sales of Peloton products, up from 14% last year. Presumably the vast majority of Peloton derived revenue is linked to the sale of stationary bikes and treadmills given their high selling prices.

As you can see, Peloton pays Affirm a simple percentage of the gross dollar value of sales (called a Merchant Fee) and gets the benefit of balance-sheet-as-a-service, if you will.

Without knowing the exact percentage paid to Affirm from Peloton sales, it is hard to know exactly how much of Peloton’s revenue is financed, but we can estimate. Given that AFRM itself has grown revenue nearly 100% YoY and Peloton’s share of that revenue has risen over 100% (from 14% to 30% share YoY), it is safe to say a vast majority of the growth at Peloton YoY was financed through Affirm.

Peloton confirms the importance of financing generally to its business model in its 10-K, but does not specifically name Affirm:

Historically, a majority of our customers have financed their purchase of our Connected Fitness Products through third-party credit providers with whom we have existing relationships.

Fulcrum of Growth

We have now established that Affirm is extremely important to Peloton. I’ll go as far as to say Affirm is THE fulcrum in the Peloton growth story.

Peloton likely cannot support this rate of growth without Affirm and Affirm’s ability to access capital is paramount to Peloton’s continued growth. Remote leverage at its finest!

If you hold Peloton, it is incumbent upon you to be aware of what is happening at Affirm. If they are unable to grow their loan book, face a credit rating downgrade or can’t get another financing round, it can ultimately impact Peloton. Yikes!

Affirm’s Achilles Heel

If I can envision one problem with Affirm it is that they may suffocate under the weight of the 0% APR loans. Think about it. Every time Peloton sells a bike, Affirm takes on another 0% APR consumer loan that it has to figure out what to do with.

These are loans that pay no interest and the only benefit Affirm sees with regard to these loans is an upfront Merchant Fee. Said another way, the 0% APR loan is a zero coupon bond, in which Affirm recognized the discount upfront as revenue and likely cannot sell along without giving back a portion of that merchant fee to finance partners.

Sadly, the revenue associated with these loans is one-time in nature while the costs are recurring. Today, Affirm says 46% of their loan book is 0% APR loans. At some point Affirm has to get rid of these 0% APR loans or suffocate under their administrative costs.

As an aside: The revenue recognition of these particular loans is aggressive. Merchant fees are recognized upon product sale, but what about loan losses? You should really net out the loss on loan purchase agreements since they are originating at 0%, getting a merchant fee and then very shortly thereafter selling that loan at a discount in a forward flow arrangement which is about 2/3 of the original merchant fee.

It is no surprise that Affirm is putting a significant number of 0% APR loans into its securitizations (see below). They are smartly selling off the 0% APR production. A great use of Other People’s Money, if I do say so myself!

Conclusion

I won’t beat a dead horse with respect to Affirm and some of the issues with their business model. The point I wanted to make was that the remote leverage provided by Affirm to Peloton is extremely important to Peloton’s growth.

Therefore, investors in Peloton need to be aware of Affirm’s business and its outlook. At the moment funding appears plentiful and a strong Affirm IPO will only bolster Peloton, but should anything impact Affirm’s ability to access capital, run - don’t walk - to the Peloton exit.